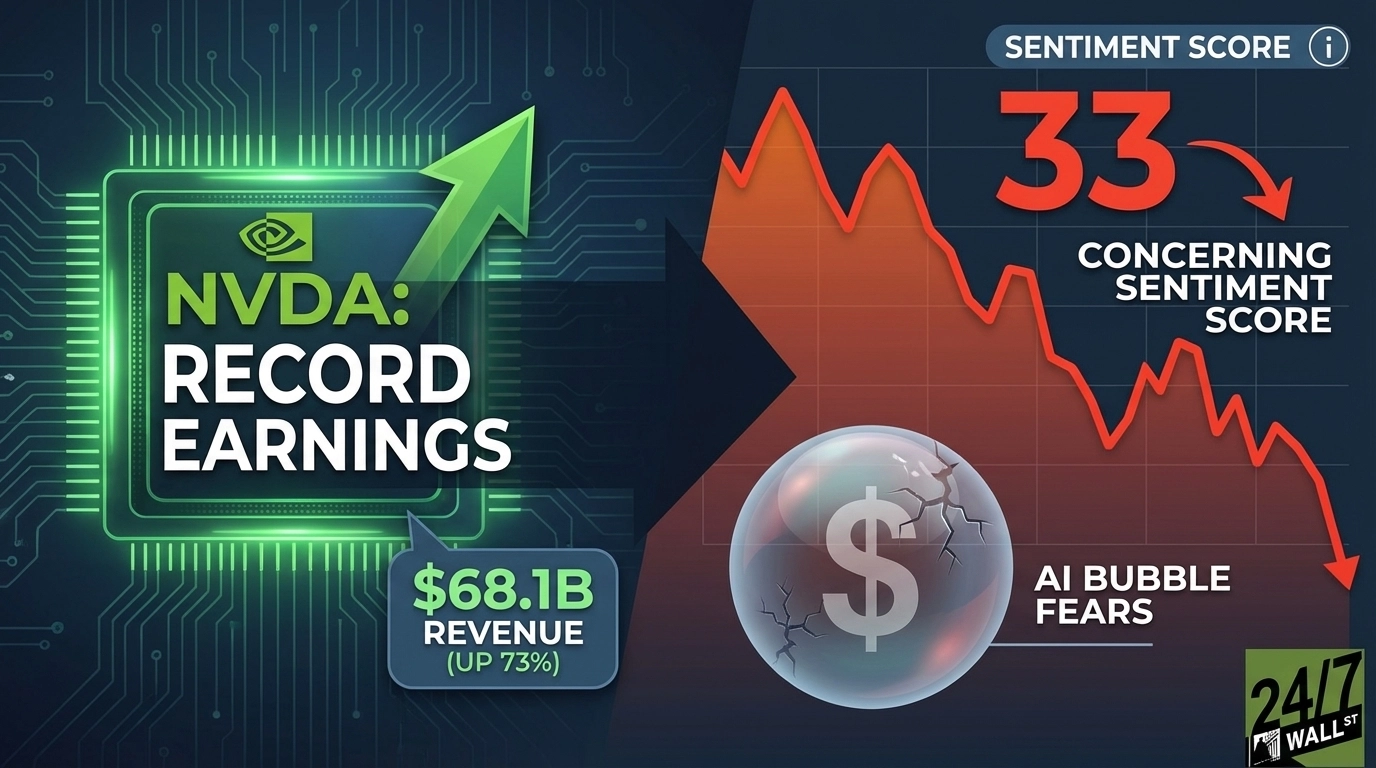

"Nvidia posted $68.1 billion in revenue, up 73% year over year, with Data Center Networking revenue surging 263% to $10.98 billion, driven by NVLink infrastructure scaling across hyperscalers. EPS came in at $1.62 against a consensus estimate of $1.52. Full-year free cash flow hit $96.6 billion."

"Forward guidance removes China entirely, reflecting export restriction risk after a $4.5 billion H20 charge in Q1 FY2026. The composite sentiment score peaked at 68 on March 3 and collapsed to 33 on March 10, a swing reflecting genuine panic. Supply commitments of $95.2 billion create real execution risk if AI spending cools."

"The most-upvoted post in r/investing came from user Dal-Thrax, whose 2,240-upvote post argued that potential government restrictions on chip sales to major AI labs represent genuine black swan territory."

Nvidia delivered extraordinary Q4 FY2026 results with $68.1 billion in revenue, 73% year-over-year growth, and $1.62 EPS exceeding consensus estimates. Data Center Networking revenue surged 263% to $10.98 billion, and full-year free cash flow reached $96.6 billion. However, the stock barely moved following the announcement, and composite sentiment scores dropped sharply from 68 to 33 within a week. Three primary concerns drive investor anxiety: forward guidance excludes China due to export restrictions and a $4.5 billion H20 charge, supply commitments of $95.2 billion create execution risk if AI spending decelerates, and potential government restrictions on chip sales to major AI labs represent significant black swan risks. This disconnect between record financial performance and market pessimism reflects deeper concerns about AI spending sustainability and regulatory headwinds.

Read at 24/7 Wall St.

Unable to calculate read time

Collection

[

|

...

]