Synopsys shares have been volatile, falling from an August 2025 peak near $617.91 to a November low of $389.83 before settling around $498.43. The stock is up over the past month and year to date, but declined in the last week and remains below its 52-week high. Q1 FY2026 results reported February 25 showed revenue of $2.41 billion, up 65.4% year over year, and non-GAAP EPS of $3.77, beating consensus. Guidance was reiterated for FY2026 revenue of $9.56B to $9.66B and non-GAAP EPS of $14.38 to $14.46. The outlook is supported by an expanded portfolio, an $11.4B backlog, improving operating cash flow, debt paydown, and a replenished buyback, while risks include China-related export restrictions.

"Synopsys enters 2026 with an expanded portfolio, leadership positions across the business, and the most compelling roadmap in our history."

"Q1 FY2026, reported February 25, delivered revenue of $2.41 billion, up 65.4% YoY, and non-GAAP EPS of $3.77, beating consensus by 5.98%. Management reiterated FY2026 guidance of $9.56B to $9.66B in revenue and non-GAAP EPS of $14.38 to $14.46."

"Bulls have plenty to point to. CEO Sassine Ghazi said "Synopsys enters 2026 with an expanded portfolio, leadership positions across the business, and the most compelling roadmap in our history." AI-fueled chip design demand is accelerating R&D spend at customers, and Synopsys carries a $11.4B backlog."

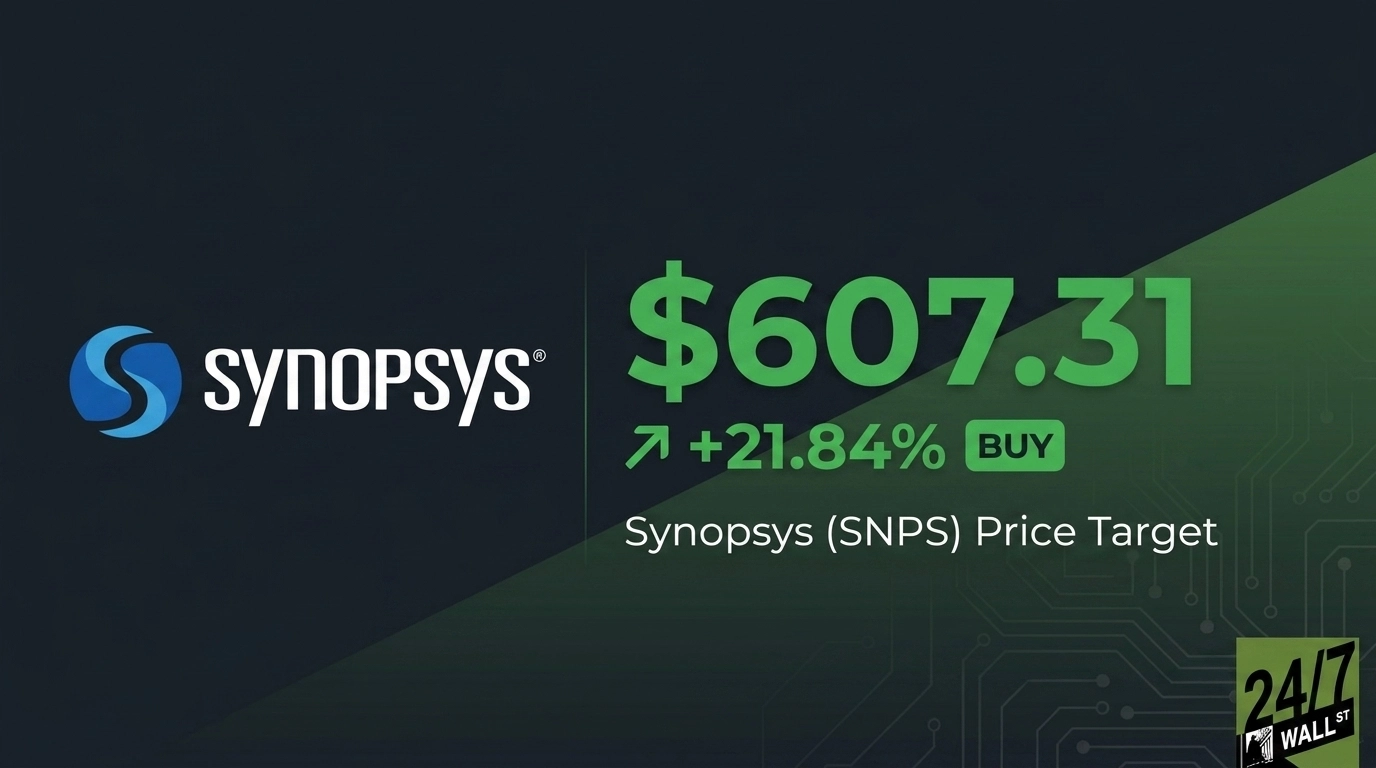

"Operating cash flow swung to $856.8M in Q1 FY2026 from negative $67M, funding aggressive debt paydown of $3.45B in a single quarter and a replenished $2B buyback. Wall Street is constructive: 15 Buy and 2 Strong Buy ratings versus 1 Strong Sell, with an average target of $537.53."

Read at 24/7 Wall St.

Unable to calculate read time

Collection

[

|

...

]