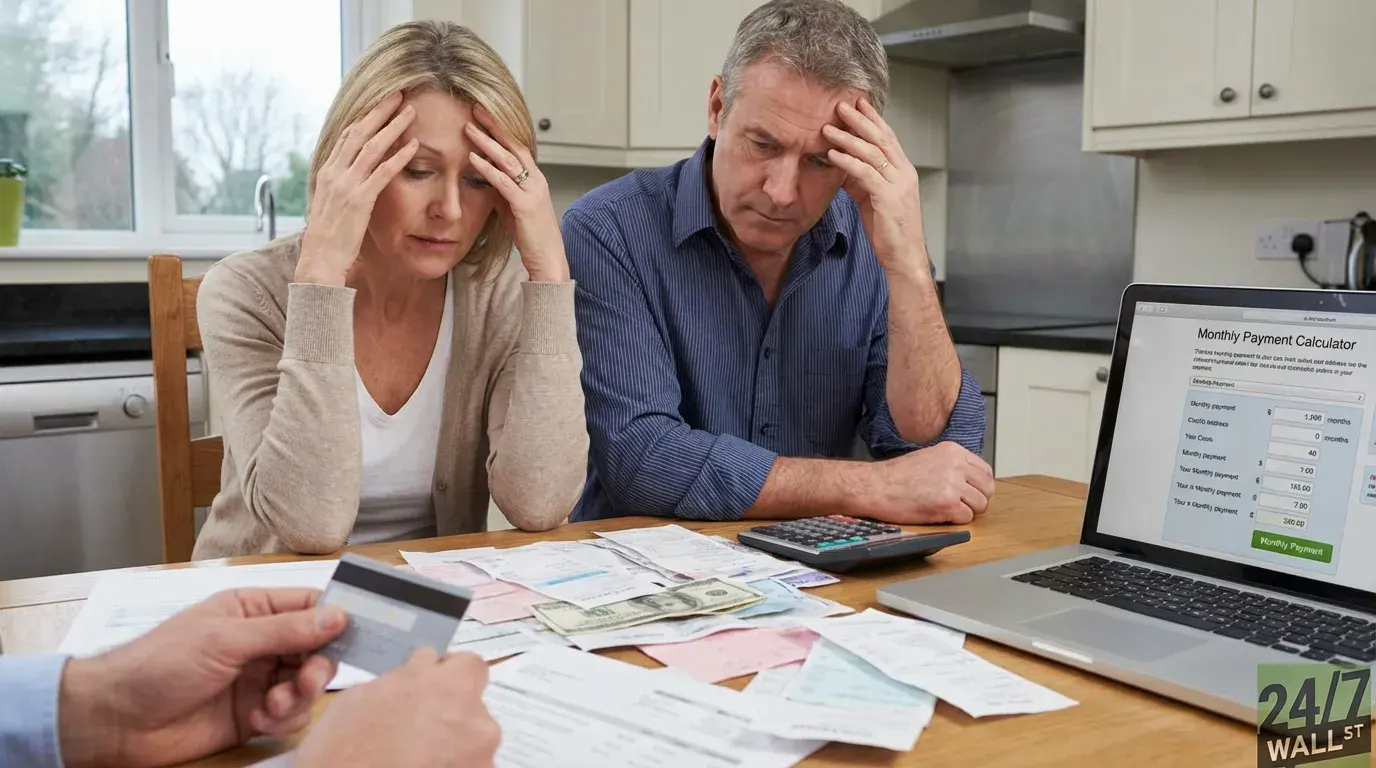

Dave Ramsey advocates an 8% annual withdrawal rate for retirees, arguing that 12% average stock market returns provide sufficient buffer. This contrasts with the 4% rule established in 1994, which has guided retirement planning for decades. For a $500,000 portfolio, 8% withdrawals mean $40,000 annually versus $20,000 under the traditional approach. While historical S&P 500 returns exceed 10% annually over the past decade, the strategy's critical weakness is sequence-of-returns risk. Withdrawing 8% during bear markets locks in losses permanently. The 4% rule survived stress-testing against the Great Depression and 1970s stagflation through balanced portfolios and margin for bad timing. Ramsey's approach assumes retiring into sustained bull markets, an assumption increasingly questionable given current economic conditions.

"A retiree withdrawing 8% during a bear market locks in losses permanently. If your $500,000 portfolio drops 30% to $350,000 and you still pull $40,000 that year, you've withdrawn 11.4% of your remaining balance. Recovery becomes nearly impossible."

"The 4% rule was stress-tested against the worst 30-year periods in market history, including the Great Depression and 1970s stagflation. It survived because it assumes a balanced portfolio and builds in margin for bad timing. Ramsey's 8% rule assumes you retire into a bull market and stay there for three decades."

"An 8% withdrawal rate means a retiree with $500,000 saved can pull $40,000 annually instead of $20,000. That difference transforms retirement from $20,000 to $40,000 in annual income for millions of households worried their nest egg won't stretch far enough."

Read at 24/7 Wall St.

Unable to calculate read time

Collection

[

|

...

]