Healthcare

fromFortune

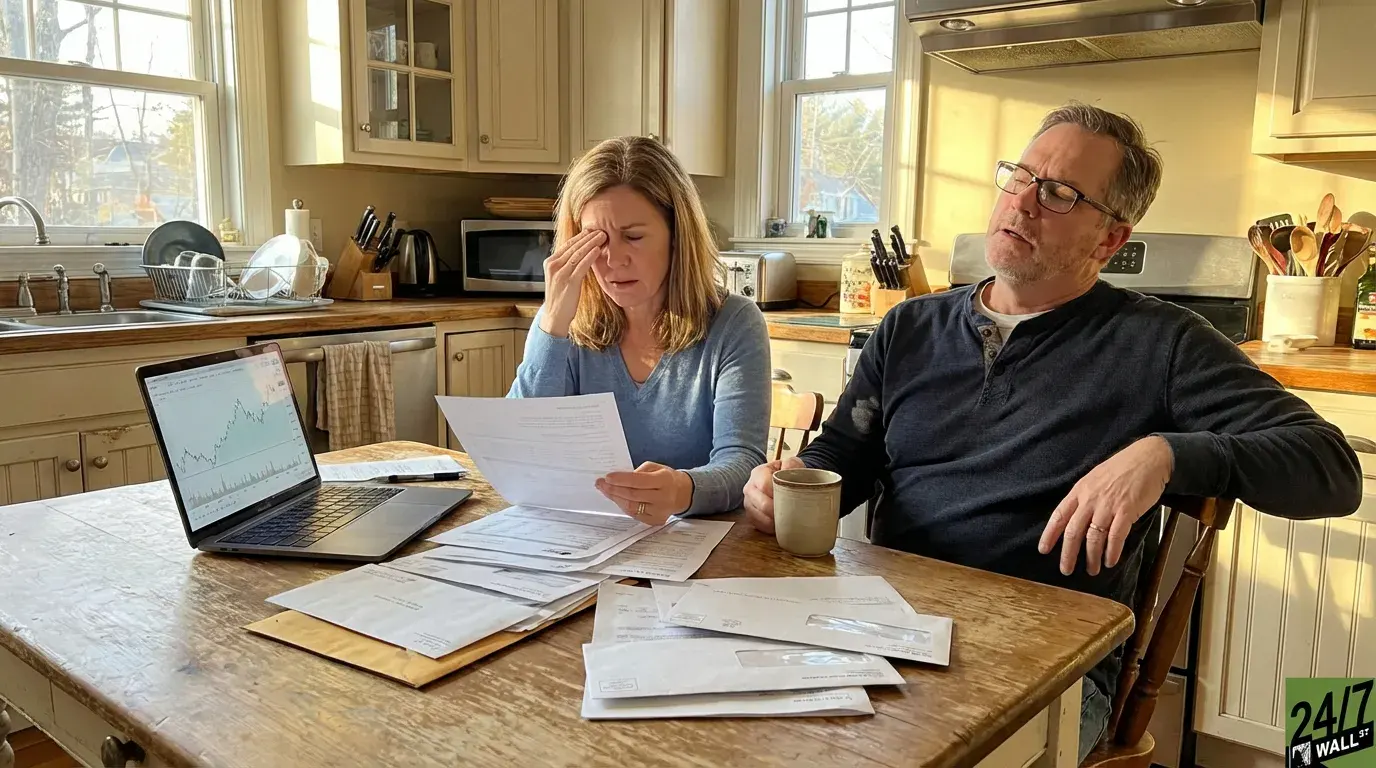

14 hours agoRetirees are facing a $345,000 bill they never saw coming - and most aren't prepared | Fortune

Healthcare costs in retirement can reach six figures, yet many do not adequately plan for them despite concerns.

Dr John Allan stated that Generation Alpha, many of whom are now approaching adulthood, are clear about what they want from their future. However, many do not feel ready for what comes next, particularly regarding the confidence, independence, and practical skills needed to navigate life after education.

The ratio of workers to beneficiaries has plummeted from 10 or more in the mid-20th century to merely two or three today. As a result, the timeline for the depletion of the program's surplus trust funds has accelerated, shifting from 2035 to the end of 2032. After 2032, incoming payroll tax revenue, income from taxation of benefits, and interest on the trust funds will not cover 100% of promised benefits.

Social Security benefits rose by 2.8% in January 2026, adding roughly $56 per month to the average retiree's check. Year-over-year inflation is running at 2.2%, which means the COLA is actually outpacing current price increases by a small margin. The catch is Medicare. Medicare Part B premiums increased in 2026, and since those premiums are deducted directly from your Social Security payment, some of that $56 gain disappears before it reaches your bank account.

A 65-year-old man today can expect to live to 84 years old, while a 65-year-old woman can expect to live until 86. For plan sponsors and advisers, that translates into a potential distribution horizon of at least 20 to 30 years. Without incorporating realistic longevity assumptions into glide path design, withdrawal strategies and income solutions, participants face a heightened risk of outliving their savings.