#financial-decluttering

#financial-decluttering

[ follow ]

#personal-finance #budgeting #financial-planning #financial-literacy #debt-management #wealth-building

Mental health

fromSilicon Canals

1 day agoPeople who grew up in houses where money was a source of tension often become adults who can afford things comfortably but still feel a small flinch at the register, and the flinch isn't financial anymore, it's a nervous system that never got the memo that the emergency is over. - Silicon Canals

Money anxiety often stems from childhood experiences rather than current financial situations, affecting emotional responses to spending.

fromApartment Therapy

21 hours agoThis "Inconvenient" Rule Actually Helps Me Keep Up with Laundry

The Inconvenient Rule involves purposely making the laundry inconvenient so that you don't put it off and let the piles grow. Since starting this method, I have felt more on top of washing, folding, and putting away clothes.

Everyday cooking

#credit-cards

Travel

fromFortune

5 days agoAmericans are credit card-maxxing tax season with sign-up bonuses while half the country relies on their refund to catch up on bills | Fortune

High sign-up bonuses on credit cards are prompting some Americans to pay taxes with new cards for points, but this strategy carries risks.

Mental health

fromSilicon Canals

2 days agoNot everyone who avoids looking at their bank account is financially irresponsible. Some people grew up in households where money conversations preceded every serious conflict, and the avoidance is a nervous system trying to prevent a fight that already happened decades ago. - Silicon Canals

Money avoidance often stems from past trauma rather than a lack of financial knowledge or discipline.

Psychology

fromSilicon Canals

4 days agoPsychology says people who grew up poor in the 1960s and 70s develop a specific relationship to waste - they can't throw away a half-used candle or a rubber band or a piece of foil, not from habit, but because their nervous system still treats abundance as temporar - Silicon Canals

Scarcity during childhood shapes the brain's stress-response architecture, leading to lasting changes in emotion regulation and threat detection.

Mental health

fromSilicon Canals

14 hours agoPsychology says the reason so many people crash emotionally in their early 60s isn't retirement or aging - it's the first time in decades they've had enough silence to hear their own thoughts and they don't recognize the person thinking them - Silicon Canals

Highly functional individuals often face delayed emotional collapse in their sixties due to decades of avoidance and relentless life pressures.

fromwww.businessinsider.com

1 day agoA full-time government employee with multiple side hustles shares his top passive income hits and flops

I always wanted to be an inventor. That's when I started really thinking about how I could bring some extra money in, but without sacrificing that safety net that I had built at my job.

Bootstrapping

#financial-anxiety

Psychology

fromSilicon Canals

1 week agoThe people who check their bank account before every small purchase aren't necessarily struggling. Some of them grew up in houses where an unexpected expense could change the entire atmosphere of a week, and the checking is not about the balance. It's about confirming that the ground is still solid. - Silicon Canals

Financial anxiety often stems from childhood experiences where money influenced household atmosphere and emotional states, not just current financial status.

Mindfulness

fromSilicon Canals

3 weeks agoPeople who grew up watching their parents check the mailbox with visible anxiety understand something about money that no financial literacy course will ever teach - that scarcity isn't a budget problem, it's a nervous system state - Silicon Canals

Financial anxiety stems from deep-rooted emotional experiences rather than just a lack of knowledge about budgeting or financial concepts.

Mental health

fromSilicon Canals

4 weeks agoThere's a specific kind of financial anxiety that has nothing to do with how much money you have. It belongs to people who finally became comfortable but never updated the internal math that was written during scarcity, so every purchase still runs through a threat calculator from 1997. - Silicon Canals

Financial anxiety often stems from past experiences rather than current financial realities, affecting decision-making even in improved circumstances.

Mental health

fromSilicon Canals

1 week agoI grew up lower middle class and the thing nobody explains is how the financial anxiety doesn't leave when the money arrives. You can have six months of savings and still feel the phantom weight of an empty account because your nervous system was calibrated in a house where the math never quite worked and it stored that frequency permanently - Silicon Canals

Chronic stress from childhood financial instability affects adult behavior and emotional responses to money.

Miscellaneous

from24/7 Wall St.

1 month agoData Shows Dave Ramsey Is Dead Wrong About This - But He Nailed One Thing

Dave Ramsey emphasizes behavioral change over mathematical optimization in debt repayment, advocating the debt snowball method despite its mathematical inefficiency compared to paying highest-interest debt first.

Psychology

fromSilicon Canals

2 weeks agoPeople who grew up calculating whether they could afford both the drink and the entree before anyone else sat down don't stop doing that math when they earn six figures. The arithmetic isn't financial anymore. It's a loyalty ritual to a younger version of themselves who promised never to be caught without an exit. - Silicon Canals

Child poverty in the U.S. leads to adult poverty more than in Denmark, Germany, the UK, or Australia, with lasting effects beyond financial circumstances.

#financial-scarcity

Mental health

fromSilicon Canals

4 weeks agoI grew up lower middle class and the thing nobody understands is that we didn't budget because we were disciplined. We budgeted because we'd already done the math on what happens when the car breaks down in the same month the insurance is due, and that math never leaves your body even after the numbers change. - Silicon Canals

Financial scarcity rewires the body and mind, creating lasting effects on budgeting and spending behaviors rooted in stress and dread.

Psychology

fromSilicon Canals

3 weeks ago7 things people raised in lower middle class households still do with money long after they can afford not to, and every single one traces back to a nervous system that learned to count before it learned to rest. - Silicon Canals

Financial habits formed in childhood persist, driven by physiological responses rather than just psychological factors.

#financial-security

Psychology

fromSilicon Canals

1 month agoBehavioral economists found that people with substantial savings who live modestly aren't being frugal - they've discovered that the security of untouched wealth provides more psychological satisfaction than any material display ever could - Silicon Canals

Financial security from modest spending and consistent saving provides greater psychological satisfaction than wealth displays or increased consumption.

Silicon Valley

fromSilicon Canals

2 months agoThe 8 money habits that quietly reveal someone grew up in a household where there was never quite enough - Silicon Canals

Childhood financial scarcity creates lasting money habits—mental tallying, stockpiling, hypervigilance, and subtle behavioral patterns that persist despite later financial stability.

fromEntrepreneur

1 month agoMindset Shift That Will Boost Your Cash Flow in 2026

Filing a return can be time-consuming and complicated. The possibility of an audit feels intimidating. And the cost can be high. Each year, Americans collectively work nearly four months just to cover their combined federal, state and local taxes. If you earn $100,000 a year, that can add up to more than $1 million over the course of your career - money that could otherwise be invested in your business or your family.

Business

from24/7 Wall St.

2 months agoThree Expensive Lessons I Learned Too Late About Money

Looking back, it's easy to spot the moments where things could have gone differently. At the time, each financial decision felt justified, and sometimes even smart! Whether it was driven by optimism, pressure, or a belief that I could "figure it out later," I made choices that seemed reasonable in the moment but were costly over time. What surprised me most wasn't just the money lost, but how similar the underlying mistakes were.

Real estate

fromBusiness Insider

2 months agoI needed to save money, so I challenged myself to a 30-day spending freeze. I learned a lot about my financial habits.

My goal was to only pay bills. I didn't want to buy anything extra, but I knew things always come up, like my son needing something for school. I told myself ahead of time that I could "break the freeze" for absolute necessities only. Over the 30 days, copays for doctor's appointments and prescription costs were the only unexpected purchases I made.

Mindfulness

from24/7 Wall St.

2 months agoDave Ramsey: "Creative Financing Just Means 'I'm Going to Do Stupid'"

Trina, a 38-year-old Florida resident, was drowning in $44,000 of debt on a $60,000 annual income. Her financial obligations spanned car loans, credit cards, and her son's private school tuition-a complex web of commitments that became more concerning when she revealed filing Chapter 7 bankruptcy just two years earlier. This recent bankruptcy suggested her struggles weren't isolated incidents but part of a recurring pattern of financial instability.

Real estate

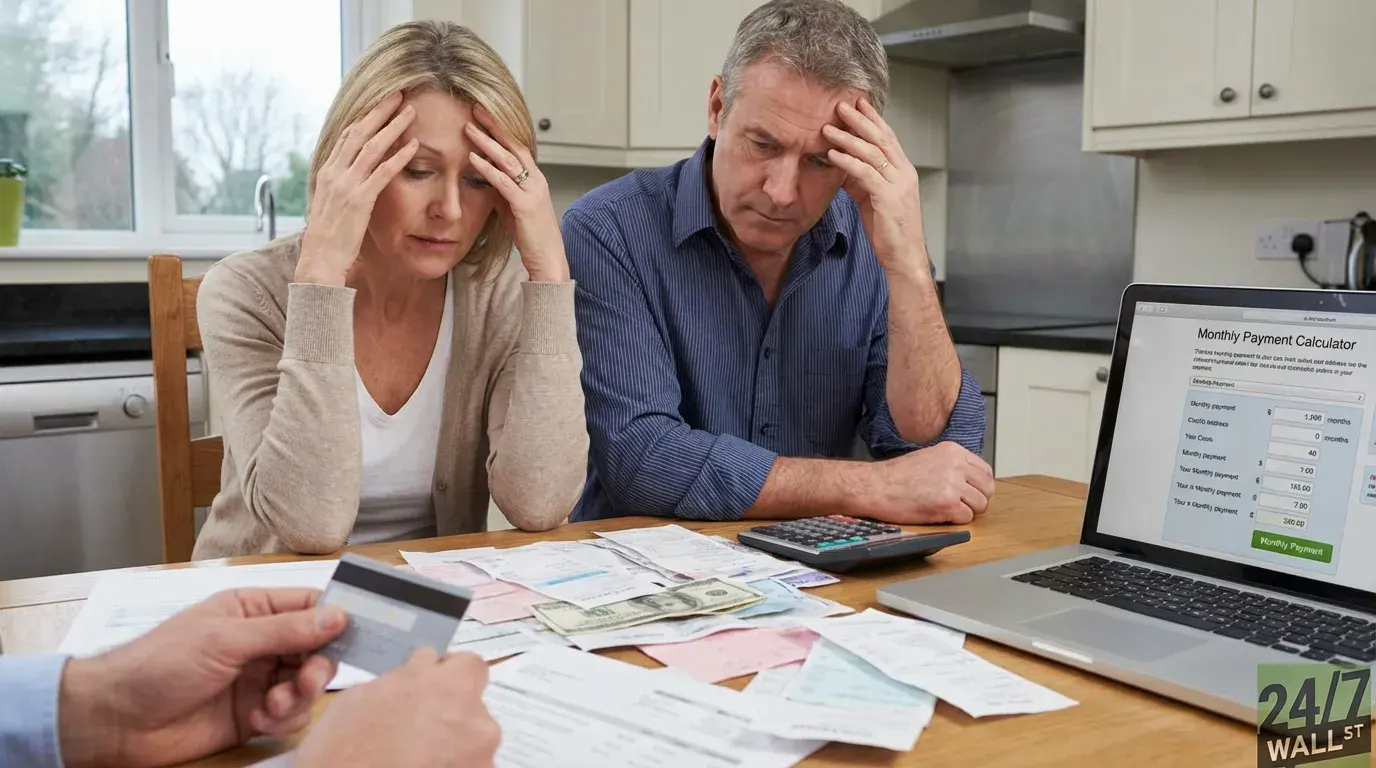

from24/7 Wall St.

1 month agoDave Ramsey: "You Can't Put $2,500 Away Because You Got $86,000 in Debt Sucking the Bone Marrow Out of Your Life"

You can't put $2,500 away right now because you got 86,000 freaking dollars in debt sucking the bone marrow out of your life. The key phrase is 'focused investing.' That only happens after the debt is gone. $2,500 per month represents exactly 15% of a $200,000 annual income. Right now, that $2,500 is not available because it's already being consumed by debt service.

Retirement

from24/7 Wall St.

2 months agoSuze Orman Says 'Get as Much Pleasure Out of Saving as You Do Spending', And She's Right

The past few years have done a number on a lot of people's savings. Between high levels of unemployment spurred by the pandemic and several years of rampant inflation, many folks have whittled down their cash reserves to practically nothing. An estimated 63% of U.S. workers did not have enough savings on hand to cover a $500 emergency expense, according to Fintech company SecureSave. That's kind of scary, though, because as a general rule, it's important to have a large enough emergency fund to cover at least three months of expenses.

Business

fromBusiness Insider

2 months agoI found dozens of recurring charges on my credit card. I had been wasting $1,600 a year on subscriptions I didn't even use.

At the beginning of the year, I looked more closely at one particular statement than I had before. I was shocked by the number of transactions I didn't recognize. They turned out to be subscriptions. My 17-year-old daughter told me that she'd been offered a special deal at the Verizon store: access to Apple Music for up to six people for $10 a month. She was desperate to take advantage of the promotion and said the streaming service had an amazing selection of songs.

Business

Psychology

fromSilicon Canals

2 months agoWhy you keep buying things you don't need-and how to stop, according to experts - Silicon Canals

Emotional states and dopamine-driven reward responses fuel impulsive, unnecessary purchases, causing repeated overspending despite awareness and intentions to save.

Psychology

fromSilicon Canals

1 month agoWhy people from lower middle class families notice small financial details that wealthier people are completely blind to - Silicon Canals

Financial hypervigilance—heightened attention to money and spending—develops in people raised in lower middle-class households and persists into adulthood, affecting how they monitor expenses and experience anxiety around finances.

[ Load more ]